A five-year review of ombudsman complaints data reveals motor insurance continues to dominate complaints volumes, while travel insurance has the highest upheld rate of the major UKGI business lines

Nearly 200,000 insurance complaints have been referred to the Financial Ombudsman Service (FOS) over the last five years – a figure that lays bare the scale of consumer dissatisfaction still facing the insurance industry.

A five-year analysis of FOS complaints data by market intelligence firm Insurance DataLab, published exclusively by Insurance Times, found that the number of insurance complaints rose over the last three months of 2024 after three consecutive quarters of falling volumes.

The increase was small – up just 0.4% on the same period a year earlier – but it was still enough to take complaints volumes to their highest levels since Q2 2023, making the end of last year one of the five busiest quarters for FOS complaints over the last five years.

This will be of concern to the UK general insurance (UKGI) industry – particularly considering the regulator’s increasing focus on customer outcomes as part of July 2023’s Consumer Duty regulation.

Most complained about lines

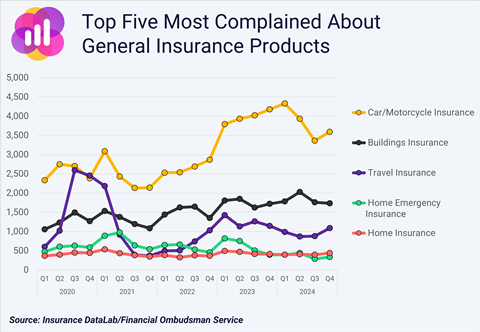

Unsurprisingly, the products with the highest number of complaints to the FOS over the five-year period included in this analysis tend to be the most commonly purchased covers.

Read: Building insurance complaints soar to record high

Read: Regulatory action warning issued as motor complaints surge

Explore more ombudsman related content here, or discover other news analysis stories here

Topping the list is car and motorcycle insurance, which generated more than 61,700 complaints and accounted for 32% of all general insurance complaints referred to the FOS over the last five years.

Buildings insurance, another widely held product, came in second spot with more than 30,600 complaints (16%). This was followed by travel insurance with 22,100 complaints (11%), home emergency insurance with 11,600 complaints (6%) and home insurance, which contributed 8,300 complaints (4%).

Combined, these five product lines accounted for 69% of all general insurance complaints handled by the ombudsman over the past five years.

The rise in motor insurance complaints will be of particular concern for many insurers. Annual complaints volumes referred to the FOS have risen by 55% since 2021 to more than 15,200 in 2024 – up from a low of less than 9,800.

This finding comes at a time when motor insurance – the biggest single business line in UKGI – is facing intense regulatory and political pressures, with the market currently under the microscope because of the motor finance commissions scandal that could see the introduction of an industry-wide redress scheme, alongside rising premiums and concerns about affordability.

Proportionate look

But the volume of complaints to the FOS tells only part of the story.

While the aforementioned products may dominate the complaint totals, the types of complaints and – crucially – the proportion upheld in the customer’s favour offer deeper insights into where the industry is struggling to deliver fair and timely outcomes.

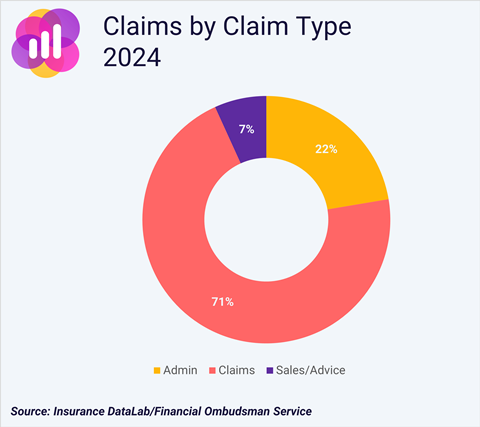

Over the most recent 12 months of FOS data, complaints relating to claims made up the overwhelming majority of general insurance referrals to the ombudsman.

According to Insurance DataLab’s analysis, 71% of all complaints in the year to the end of 2024 were claims related, compared to 22% concerning administrative issues and just 7% relating to sales or advice.

This breakdown has remained largely consistent across multiple reporting periods and reflects a long-standing issue within the insurance industry – that many policyholders only fully engage with their insurer when making a claim and that it is this part of the experience that ultimately shapes their perception of value and fairness.

Insurance DataLab co-founder Dan King said the claims experience had become an even greater test of insurer performance under Consumer Duty.

He explained: “Given the importance of this interaction, the high proportion of claims related complaints highlights how much work remains to be done across the industry.

“Whether the issues relate to delays in processing, lack of communication, disputed decisions or a failure to meet expectations, our analysis demonstrates that many insurers are still struggling to deliver the kind of claims journey that builds trust and confidence in their brand and the wider industry.”

Complaints upheld

Equally significant to the most commonly complained about lines and the type of complaints is the question of how many of these complaints are upheld in favour of the customer – a key marker of whether insurers are taking the right decisions in the first place, or whether claimants are being forced to fight for fair outcomes.

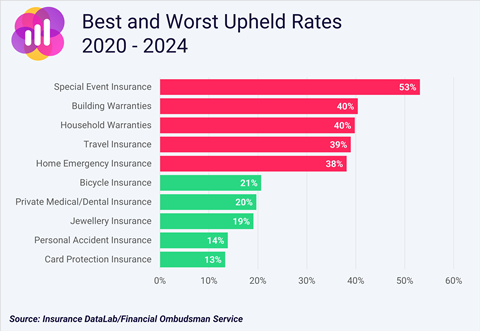

Some of the most striking findings in this five-year analysis come from smaller product lines that have recorded consistently poor upheld rates.

Special event insurance recorded the worst performance of any line for this metric, with 53% of complaints about this product upheld by the ombudsman, meaning that insurers have made the wrong decision in more than half of all complaints.

Two further business lines that performed poorly here were building warranties and household warranties, both of which had average upheld rates of 40%.

More worryingly for UKGI, two of the five product lines with the highest upheld rates – travel insurance and home emergency insurance – also ranked among the most complained about product lines.

Travel insurance posted a 39% upheld rate across almost 22,100 complaints, while home emergency insurance had nearly 11,600 complaints with an upheld rate of 38%.

This combination of high volumes and high upheld rates makes these two lines especially exposed to regulatory and reputational risk. It also raises questions about the suitability of policy design and the effectiveness of claims handling in these areas.

Some product lines, however, show insurers are getting it right more often.

The FOS’ data highlighted several product lines that have recorded relatively low upheld rates – a sign that while complaints still arise, insurers are generally managing to resolve them fairly and in line with policy terms.

Card protection insurance, for instance, recorded the lowest upheld rate of any business line over the past five years, with just 13% of complaints being upheld by the FOS.

Other strong performers included personal accident insurance with an upheld rate of 14%, jewellery insurance (19%), private medical and dental insurance (20%) and bicycle insurance (21%).

These products tend to be more niche in nature, with smaller policyholder bases and more narrowly defined cover. While that may contribute to a lower complaint rate, it also allows for greater clarity in the customer relationship and a more targeted approach to claims.

Nonetheless, there may be lessons that can be drawn from how these products are structured, communicated and serviced – particularly in terms of managing customer expectations and delivering consistent outcomes.

Regulatory toolkit

For King, these upheld rates and complaint volumes are much more than just customer satisfaction metrics – they are increasingly becoming part of the regulatory toolkit for assessing insurer performance.

He said: “Since the introduction of Consumer Duty, insurers are now expected to demonstrate that they are actively delivering good outcomes for their customers, not merely avoiding poor ones.

“Complaints data is a key element of how those outcomes will be measured by the regulator. That’s why we work closely with insurers to ensure they are aware of how they are performing relative to their peer group and the wider market, [as well as] to highlight areas of improvement before they become a serious issue.”

King added that data driven insight will be critical to helping insurers stay ahead of regulatory intervention.

He explained: “The regulator will be looking for outliers that are delivering high levels of underwriting profits while also demonstrating poor outcomes with large volumes of complaints and high upheld rates.

“We can only see the FCA getting more interventionalist over the coming months, so it is essential that insurers know if there are any issues within their books of business ahead of time.”

As industry-wide competition intensifies and switching provider becomes easier, customer loyalty is increasingly fragile. Poor complaints performance, therefore, can also undermine even the strongest brand positioning, while high upheld rates can lead to avoidable costs that put pressure on an insurer’s bottom line.

In the end, the challenge for insurers is not simply to bring down complaint volumes, but to deal with complaints fairly, consistently and early – reducing escalation, protecting reputation and, most importantly, restoring consumer trust.

In a market where consumer expectations are rising and tolerance for poor service is falling, trust is no longer a soft metric – it is the new competitive advantage.

No comments yet