Companies rated as a top 50 insurer by GWP are falling behind smaller, more specialised operators when it comes to COR scores

Insurance Times’ Top 50 Insurers report, published in October 2024, features the largest non-life insurers across the whole of the UK and Gibraltar, controlling almost £80bn of gross written premium (GWP).

But what role does size play when it comes to delivering profitable underwriting results?

To help answer this question, market intelligence firm and Top 50 Insurers data provider Insurance DataLab analysed the latest underwriting results of the non-Lloyd’s insurers in this year’s report and compared them against the rest of the market.

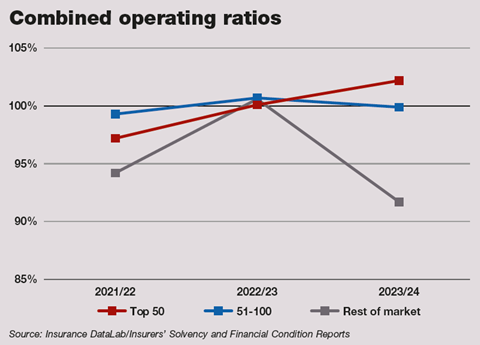

Based on each insurer’s latest Solvency and Financial Condition Report (SFCR), the 2024 cohort of the UK’s largest general insurers reported an aggregate combined operating ratio (COR) of 102.2% for 2023/24. This marks the second consecutive year for which the top 50 firms have collectively recorded an underwriting loss, after two years of deteriorating underwriting results and an aggregate COR of 101.1% for 2022/23.

This year’s cohort of top 50 insurers is also the first to report a higher COR than those insurers outside the UK’s 50 largest insurance groups since 2020/21.

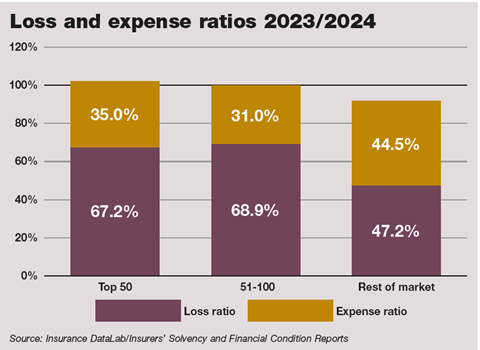

Insurers outside the top 50 reported an aggregate COR of 99% in their latest SFCRs. This is some 3.2 percentage points better than the insurers named in the Top 50 Insurers report and it also represents a 1.7 percentage point improvement on last year’s 100.7% COR.

Indeed, the underwriting results of the non-life insurers that make up the UKGI marketplace improve more impressively outside the top 50 firms.

The insurers placed 51 to 100 by GWP reported an aggregate COR of 99.9% for 2023/24 as they returned to underwriting profit after a loss-making 100.7% COR year. Meanwhile, the insurers outside the 100 largest firms reported an aggregate COR of 91.7% in the last reporting period, down from 100.6% and some 10.2 percentage points ahead of the aggregate position for the market as a whole.

Losing less

A lot of this outperformance will be driven by the more specialist nature of the insurers outside the top 50 insurers, with larger insurers often operating in more mainstream markets that can deliver greater volume, even if that is at the expense of underwriting profit margins.

This is most clearly seen in the performance of insurers outside the top 100, which reported an aggregate loss ratio of just 47.2% for 2023/24. This is more than 20 percentage points better than their larger peers and is a major driver of their improved underwriting performance. Indeed, those insurers placed 51 to 100 by GWP achieved an aggregate loss ratio of 68.9%, while the top 50 firms reported a loss ratio of 67.2%.

It is worth noting, however, that the specialised nature of these smaller insurers is not always a benefit, with a lack of diversification leading to a much more volatile loss ratio – the standard deviation of the loss ratio for these smaller insurers is 6.8% over the past three years, compared with just 4% for the market as a whole.

Expenses is a different matter, however, with smaller insurers not able to benefit from the economies of scale that come with having a bigger book of business.

This is evidenced by an expense ratio of 44.5% for 2023/24, compared with an average of 34.7% for the market as a whole. Indeed, these smaller insurers have reported a higher expense ratio than their peers each year since Insurance DataLab started this analysis four years ago.

Insurers outside the top 100 were also the only cohort of companies to report a worsening expense ratio over the past 12 months, with the aggregate ratio for these companies rising 4.5 percentage points from 40% last year.

Those featured in the Top 50 Insurers, meanwhile, knocked 1.5 percentage points off their expense ratio to 35%, while the insurers ranked between 51 and 100 by GWP improved their expense ratio by four percentage points for an aggregate ratio of 31%.

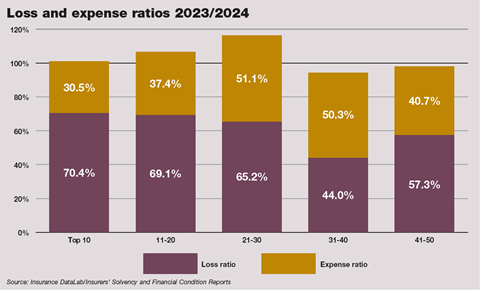

But while there is a difference in performance for those inside and outside the top 50 ranking, what difference does size make for those insurers that did make this year’s list? Unsurprisingly, the economies of scale that appear across the market are also seen within the top 50 insurers, with the 10 largest insurers in this year’s research reporting the lowest expense ratio – at just 30.5%.

This outperformance has been delivered in each of the past four years, with these insurers clearly benefiting from operating with a much larger premium base and within a larger group structure that allows for more centralised operations in certain areas. Indeed, of the nine non-Lloyd’s insurers that feature in the top 10, only two – Hiscox and Direct Line Group – reported an expense ratio higher than the market average.

Conversely, these larger insurers were not as strong when it came to the loss ratio, with an average of 70.4% – some 3.3 percentage worse than the market average, with only three reporting a better than average loss ratio.

Despite this, the low expense base from which they operate meant that six of the nine non-Lloyd’s insurers in this year’s top 10 were still able to report a profitable COR for 2023/24, although particularly poor performances from two of the three loss-making insurers did mean that this group fell to an aggregate loss with a COR of 100.9%. This was, however, still ahead of the average COR for the top 50, with only those insurers ranked 31 to 40 and 41 to 50 reporting a better COR.

This outperformance by insurers placed at the lower end of the top 50 is primarily driven by a better than average loss ratio, with insurers in the bottom half of the table reporting a higher aggregate expense ratio than those placed higher up the ranking.

As with the wider market, these smaller insurers are also much more likely to operate in specialised and niche markets.

And while high expense ratios are still limiting overall profitability for these players, the rise of generative artificial intelligence (AI) – and the corresponding availability of much cheaper technology tools – could soon start to close this gap and make these operators a much stronger force. It will be interesting to see how this affects profitability in next year’s edition of the Top 50 Insurers.

No comments yet