Motor and transport insurance remains the most complained about business line in UKGI, according to the FCA, with complex claims and repair delays fuelling frustrations

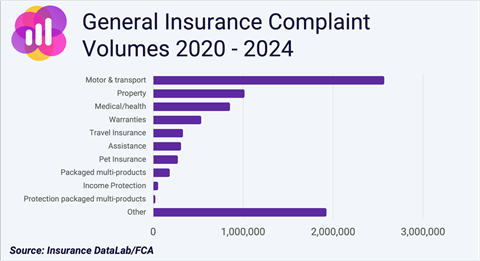

Motor and transport insurance continues to be the most complained about business line in UK general insurance (UKGI), accounting for almost a third of all complaints over the course of the last five years.

That is according to analysis of FCA complaints data by market intelligence firm Insurance DataLab, published exclusively by Insurance Times.

The FCA publishes complaints data twice a year, every six months – typically in April and October. This includes submissions from firms reporting 500 or more complaints within a six-month period, or firms reporting 1,000 or more complaints in a year.

Over the last five years, consumers lodged more than 2.5 million complaints about motor and transport insurance – equal to 32% of total recorded complaints.

This is more than double the volume of complaints received by the second most complained about business line – property insurance – which recorded nearly one million complaints over the same reporting period. This is equal to 13% of total complaints volume.

Insurance DataLab co-founder Dan King said this data demonstrated how dominant motor insurance was in the complaints landscape.

He explained: “The scale of motor complaints really sets it apart from the rest of the market. Even five years on from the Covid-19 pandemic, [this line of business] continues to generate more than double the number of complaints than any other product line.”

King added that Insurance DataLab’s separate analysis of Financial Ombudsman Service (FOS) data showed that around two-thirds of motor complaints relate to the claims process, pointing to deeper issues at the heart of the UK’s largest insurance market.

“These large complaints volumes are partly down to the sheer volume of policies sold in the motor market, but it is also a symptom of the rising complexity and cost of claims,” he said.

“Cars and other vehicles continue to get more technologically advanced. This, combined with the issues seen across the repair network and a general lack of capacity, is creating further issues for consumers – and driving more complaints.”

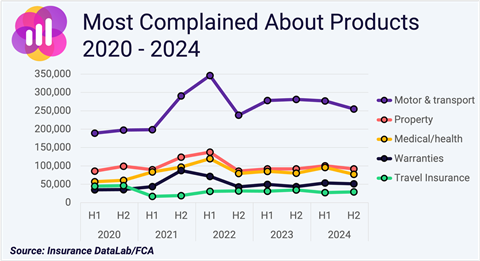

The other products making up the five most complained about business lines in UKGI are medical and health insurance, with 835,000 complaints over the last five years, warranties, which recorded 515,000 complaints in this period, and travel insurance, with 315,000 complaints.

As a percentage of overall complaints volume, these numbers equate to 11%, 7% and 4% respectively.

These figures mean there have been almost 7.9 million complaints made about insurance companies over the last five years, with total redress totalling more than £637m.

The average amount of redress paid out per complaint now stands at £77.06. While this is down from a high of £112.07 in H1 2022, it is still considerably higher than the £60.58 low reported for H2 2019.

“Rising redress levels demonstrates how the cost of resolving complaints is increasing, despite falling volumes,” King said. “This could reflect inflationary pressure on claims or a shift toward more complex, higher value disputes.”

Trend analysis

Despite the large complaints volumes and redress amounts seen across the market – not just in motor insurance – it is important to note that complaints volumes have been falling in recent months.

Total complaint volumes year-on-year have fallen in four of the last six half-year periods, although it is worth noting that complaints spiked in 2021 in the wake of the Covid-19 pandemic.

Read: Ombudsman complaints reveal insurers are still struggling with claims

Read: Which? demands FCA action as insurers ‘fail to meet’ Consumer Duty standards

Explore more insurer related content here, or discover more news articles here

Total complaints volumes overall are down 12% in H2 2024 compared to five years earlier – but redress has increased 14% to nearly £55m for the final six months of 2024.

This picture is not consistent across all business lines, however, with several products experiencing significant increases in complaint volumes compared to five years ago.

Among the product lines with over 100,000 complaints since 2020, warranties saw the largest increase – up 68% to more than 50,000 in H2 2024, compared to just over 30,000 complaints five years earlier.

Medical and health insurance complaints, meanwhile, rose 39% over this same reporting period, while pet insurance and packaged multiproducts both increased by 38%.

It is also worth noting that among the five most complained about business lines, only property insurance saw a decline in complaints since 2019 – falling 10%.

Understanding upheld rates

When it comes to assessing complaints performance, it is also important to look at upheld rates – the proportion of complaints that are found in favour of the customer. On this measure, the industry has started to show signs of improvement.

The upheld rate across all lines, excluding payment protection insurance (PPI), stands at 57.3% for the last six months of 2024.

While this represents a slight improvement on the 57.8% upheld rate for the same period in 2019, it is much improved on the three-year period between 2021 and 2023, when the upheld rate broke through the 60% barrier and peaked at 67% in the first half of 2022.

King said the industry should take encouragement from the recent drop in upheld rates

“There are early signs that insurers are making progress in resolving more complaints to the customer’s satisfaction before they need to be escalated,” he said. “The improvement from the 2022 peak shows a move in the right direction – but there’s still work to do to keep this trend going.

“One of the most effective ways to maintain this progress is through regular benchmarking. By comparing complaints performance with peers, insurers can identify areas for improvement and adopt best practices from across the market.”

Service slowdown

Insurers have, however, been getting slower at handling complaints – something that will be of market-wide concern given the delays seen elsewhere in the value chain when it comes to resolving claims, driven by the cost of living crisis and the shortage of capacity in the repair network.

The proportion of complaints being resolved within three days of being raised fell to 45.9% in the last six months of 2024, down from a high of 53.2% in H2 2021.

The proportion of complaints closed within eight weeks but after an initial three days, meanwhile, has risen to 49.9% – the highest level since Insurance DataLab started analysing FCA complaints figures.

King said this slowdown in complaint resolution times could risk undermining recent progress in other areas.

“Speed is a vital part of good customer service and delays in resolving complaints can add to frustration and harm trust,” he said.

“Insurers need to balance improvements in upheld rates with faster resolution times, especially during a period of strain on the wider claims infrastructure.”

With overall complaint volumes heading in the right direction, but service challenges persisting, the figures highlight the need for insurers to maintain momentum on customer service improvements – particularly as regulatory scrutiny and consumer expectations continue to rise.

Those insurers that get this right will be setting themselves up for a successful future, while those that fail to take the right action could find themselves lagging behind – potentially with the regulator waiting in the wings.

No comments yet