Market intelligence firm emphasises that ‘insurers need to do better to prevent complaints from happening’ as redress payments increase

Health insurers feature heavily on the list of the most complained about insurers in UK general insurance (UKGI), according to the latest analysis of FCA complaints data by market intelligence firm Insurance DataLab.

This analysis, published exclusively by Insurance Times, found that three of the five most complained about insurers over the first six months of 2024 are specialist health insurers.

Axa PPP Healthcare tops this list of the most complained about insurers, receiving 36.75 complaints for every 1,000 policies in the first half of 2024, while Unum came second with a rate of 19.12.

Meanwhile, fellow health insurer Bupa Insurance ranked fourth with 10.08 complaints per 1,000 policies – just behind Saga Services with a rate of 10.65 and marginally ahead of British Gas Services, which recorded a complaints rate of 9.94 per 1,000 policies.

This compares to an industry average rate of just 4.59 complaints per 1,000 policies – although this is up from 4.28 for H1 2023.

Insurance DataLab also reviewed the FCA’s complaints figures for the 10 largest insurers by gross written premium (GWP) – this presented a very different picture, with the majority of these insurers performing much better than the industry average.

Aside from the health insurance outliers of Axa PPP Healthcare and Bupa Insurance, only Axa Insurance UK and UK Insurance, more commonly known as Direct Line Group, reported a complaints per 1,000 policies rate higher than the industry average, recording 9.45 and 5.51 respectively.

At the other end of the spectrum, Allianz Insurance was the best performing insurer in this cohort, reporting just 0.69 complaints per 1,000 policies, ahead of AIG UK at 0.86.

While complaint volumes are an important metric, it is also essential to consider upheld rates – the proportion of complaints that are upheld by the insurer in favour of the customer.

Axa PPP Healthcare, which received the highest level of complaints, had the lowest proportion of complaints upheld at 47.99%, closely followed by Liverpool Victoria with an upheld rate of 48.19%. AIG UK had the third lowest upheld rate at 53.99%.

Meanwhile, UK Insurance had the highest upheld rate at 70.29%, followed by NFU Mutual with 62.51%. Aviva Insurance and Allianz Insurance both recorded an upheld rate of 61.30%.

Trend analysis

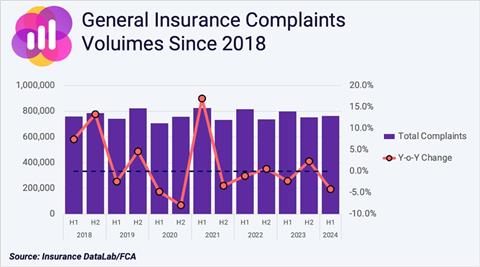

Insurance DataLab’s analysis of the aggregate FCA complaints data also revealed that overall complaints volumes have been falling.

Insurers handled a total of 764,524 complaints in the first six months of 2024 – this is a 4.2% fall on the 797,864 complaints recorded for H1 2023.

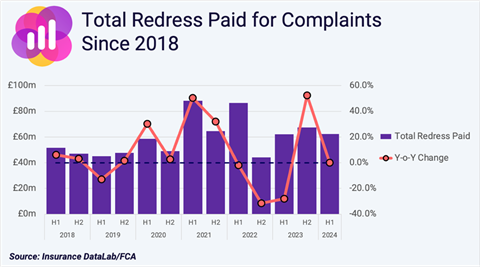

However, the total redress paid by insurers rose slightly in H1 2024 to £62.3m, compared to £62.2m during the same period last year.

This brings the average redress payment to £81.42 for 2024’s first half – 6% higher than the £76.81 recorded for H1 2023.

Despite this increase, the average redress remains well below its peak of £112.07 in H1 2022, although it continues to sit above pre-pandemic levels.

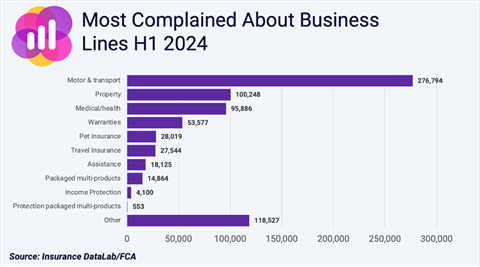

Motor and transport insurance continues to be the most complained about product line in UKGI, receiving a total of 276,794 complaints in the first half of 2024. This represents a slight decrease of 0.4% from the 278,034 complaints recorded for the same period last year.

Motor insurance alone accounted for more than twice the number of complaints received by any other business line, while property insurance ranked second with 100,248 complaints – up 8.9% from the previous year.

Five business lines experienced rising complaints overall in 2024’s first half, with medical and health insurance leading the way. This sector saw a 12.4% increase in complaints to 95,886 – this makes it the third most complained about insurance product in the UK.

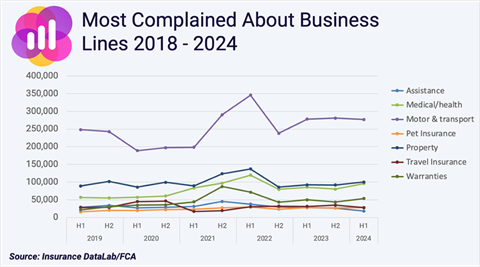

In contrast, travel insurance – which saw a spike in complaints volumes during the Covid-19 pandemic – reported an 11.9% drop in complaints over the first half of this year, down to 27,544 compared to 31,987 for 2023’s H1.

This is much closer to pre-pandemic levels, where travel insurance complaints averaged 26,696 per six-month period between 2017 and the end of 2019. Travel insurance is now ranked sixth in terms of complaints across all business lines.

When it comes to redress, however, travel insurance ranked third according to the FCA’s data, with £31.5m paid out in H1 2024. This is just behind property insurance at £40m, with the average amount paid in redress much higher in this business line compared to others in UKGI.

Unsurprisingly, motor and transport insurance topped the redress charts, mainly due to the sheer volume of complaints the product line receives.

Over the past five years, motor insurers have paid out more than £3.2bn in redress, demonstrating just how costly getting these decisions wrong can be for insurers.

It is worth noting, however, that in the first half of 2024, redress in this line of business fell by 1.7% to £702.4m – down from £716.4m for the same period in 2023.

Despite this improvement, this number is still higher than the redress recorded by motor insurers for all periods prior to the second half of 2022.

The £690.1m redress paid out by motor insurers in 2022’s second half marked the first time that this figure had totalled more than £500m for this line of business.

Generating a ‘win-win’

Across the market as a whole, it is encouraging to see complaint volumes coming down – although the lack of a corresponding decrease in redress payments will be a cause of concern for the industry.

However, overall complaints volumes still remain high, signalling persistent issues within the industry. Insurance DataLab co-founder Dan King therefore believes that insurers must prioritise not only effective complaints handling, but also proactive measures to prevent complaints occurring in the first place.

“The insurance industry continues to suffer from a poor reputation and insurers can help to address this through solving some of the key pain points that customers continue to face,” he said.

“Whether it be confusing user journeys with unnecessarily complicated language, or slow claims processes that don’t deliver quickly enough when it matters, insurers need to do better to prevent complaints from happening.”

And King highlighted that customer education is one area where insurers could make a real difference.

“Many of the problems facing the industry stem from consumers not understanding what is and isn’t covered by their policy,” he continued.

“The insurance industry needs to do a much better job of explaining this and clarifying any exclusions before the policy is purchased.

“By doing this, not only can insurers help to reduce the volume of complaints they receive – and the corresponding reduction in cost – but they can also foster greater customer loyalty and improve the public perception of the industry as a whole.

“And that’s a win-win for everyone.”

No comments yet