Data from Insurance DataLab reveals the green shoots of profitable recovery for UK, but what is driving it?

Insurance DataLab’s latest analysis of the five largest business lines in UKGI reveals a market that has emerged from one of its toughest underwriting periods in recent memory, with motor and property leading a significant improvement in profitability.

This new research, published exclusively by Insurance Times, studied Solvency and Financial Condition Reports (SFCRs) from insurers across the UK and Gibraltar, finding that each of the five largest business lines by gross written premium (GWP) generated an underwriting profit for 2025/26.

Although profitability remains under pressure in some areas, the market has staged a notable recovery over the last three years.

Outside these core markets, specialist classes continue to deliver the strongest underwriting margins. Legal expenses reported a combined operating ratio (COR) of just 67.8% for 2025/26, while credit and suretyship achieved 68.7% and assistance reported 87.1%.

However, these remain significantly smaller markets than the UK’s largest commercial and personal insurance classes.

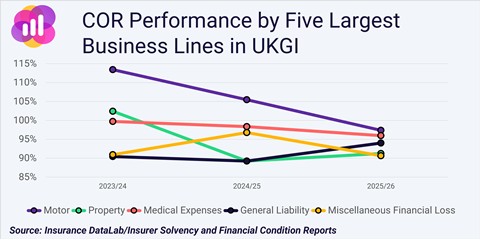

Motor remains the largest business line in UKGI and has also delivered the most dramatic improvement.

Just three years ago, the market reported a highly unprofitable COR of 113.4%, equating to an underwriting loss of more than £1.5bn. The combination of claims inflation, rising repair costs and intense pricing pressure pushed underwriting performance to one of its weakest levels in recent years.

The picture has improved steadily since then.

The aggregate COR fell to 105.5% for 2024/25 before dropping below the 100% breakeven point, reaching 97.4% for 2025/26. As a result, the market generated an underwriting profit of almost £396m.

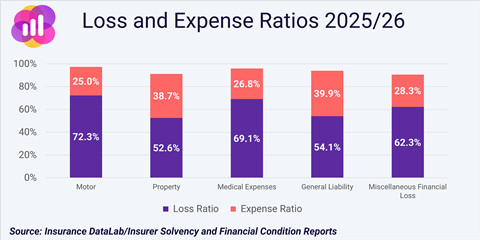

Much of the improvement has been driven by claims performance. The aggregate loss ratio has fallen from 85.7% to 72.3% over this same period, driven by an 8% drop in net claims incurred from 2024/25 to 2025/26.

Meanwhile insurers have also continued to improve operational efficiency, reducing the expense ratio from 27.7% to 25.5%.

The recovery has been evident across both personal and commercial motor business, with commercial motor insurers now outperforming their personal lines peers.

Commercial motor insurers reported a COR of 95.6% for 2025/26 – a 9.9 percentage point improvement on the previous year – while personal lines motor insurers reported a COR of 97.8% in the latest set of SFCRs, down from 105.4%.

Improved fortunes

Property insurance has also reported improved fortunes in recent years.

Read: Claims performance comes into sharper focus as brokers seek placement certainty

Read: The most complained about business lines in UKGI

Explore more Data Matters content here, or discover other news analysis stories here

Having reported a loss-making COR of 102.4% for 2023/24, the market returned to profitability the following year with an 89.2% COR before this rose slightly to 91.2% for 2025/26.

Despite this modest deterioration, property remains one of the strongest-performing large business lines, reporting an aggregate underwriting profit of more than £830m for 2025/26 – the largest in UKGI and a marked turnaround from an underwriting loss of almost £213m just two years earlier.

Claims costs have continued to improve, with the aggregate loss ratio falling from 59.9% to 52.6% over that same period. Although the expense ratio increased to 38.7% for 2025/26, following an exceptionally strong performance the previous year, it remains comfortably below the 42.5% reported in 2023/24.

The difference in performance between commercial and personal lines is more marked in the property market compared to motor insurance, however.

Commercial property continued to outperform personal property, reporting a COR of 84.9% for 2025/26 compared with 98.6% for personal lines.

While motor and property have attracted much of the attention in recent years, medical expenses has quietly produced one of the most consistent improvements across the major business lines.

The market moved from a near-breakeven COR of 99.7% for 2023/24 to 98.4% the following year before improving further to 96.0% for 2025/26.

This translated into an underwriting result of more than £268m, compared with just £18m three years earlier.

The improvement has been driven by a combination of stable claims experience and gradually improving operational efficiency, with the loss ratio falling from 70.9% to 69.1% and the expense ratio improving from 28.8% to 26.8%.

Although less dramatic than the recovery seen within motor, medical expenses has steadily strengthened its underwriting position throughout the period.

Characteristic consistency

General liability business has also continued to demonstrate the consistency that has characterised the market over recent years.

The business line remained comfortably profitable throughout the three-year period, reporting CORs of 90.4%, 89.2% and 94.0% respectively, although performance has deteriorated for 2025/26.

Indeed, the aggregate underwriting result almost halved for 2025/26, falling from £473m to £239m as expenses increased and net earned premiums fell as premiums continued to soften.

The market’s loss ratio improved slightly from 55.6% in 2024/5 to 54.1%, but this was more than offset by the expense ratio rising by 6.3 percentage points to 39.9%.

Within the wider liability market, public and products liability remained the strongest-performing segment with a COR of 88.1%, outperforming employers’ liability at 91.7%, while professional indemnity and other general liability reported CORs of 97.5% and 98.4% respectively.

Miscellaneous financial loss has remained one of the more profitable large business lines – reporting the best COR of the five largest business lines in this analysis – although its performance has fluctuated more than some of its peers.

Even so, miscellaneous financial loss has remained consistently profitable throughout the period, never reporting a COR above 97%, unlike motor and property, which both spent part of the period in underwriting loss.

The market reported a COR of 90.9% for 2023/24 before weakening to 96.8% in 2024/25 as claims and expenses increased. It subsequently recovered to 90.7% for the latest reporting period.

That improvement helped drive the underwriting result to more than £201m, more than double the previous year’s figure.

Unlike several other business lines, however, the recovery has been driven primarily by a sharp improvement in expenses rather than claims performance.

The aggregate expense ratio fell from a high of 38.99% in 2024/25 to 28.3% in the latest set of SFCRs following a sharp reduction in expenses, which helped to offset a rising loss ratio after net earned premiums fell more sharply than net claims incurred.

Green shoots

Taken together, the figures suggest the UK’s largest general insurance markets have moved beyond the severe underwriting pressures experienced during the recent inflationary cycle.

Motor and property have led the recovery, both returning to healthy underwriting profitability after recording significant losses just a few years ago, while medical expenses has steadily strengthened and general liability has continued to deliver consistent profits despite some recent deterioration.

Although specialist classes such as legal expenses and credit and suretyship continue to deliver strong results, the return to profitability across the market’s largest business lines is perhaps the clearest indication yet that underwriting conditions have normalised after one of the most challenging periods the sector has faced in recent years.

Despite this recovery, geopolitical uncertainty, persistent claims inflation and a softening rating environment are likely to keep pressure on underwriting profitability.

Whether the market can sustain its recent improvement may depend on insurers maintaining underwriting discipline as competition intensifies.

No comments yet